Welcome to The Margin, a newsletter designed to keep you on the leading edge of monetization.

In business, the difference between being ahead of the curve or slow to adapt is anything but marginal. The Margin aims to be the most useful, timely, and incisive ping that hits your inbox all week. It includes critical research and analyst insights to inform short and long-term decision making.

Research Spotlight

Is the IPO Market Opening? |

|

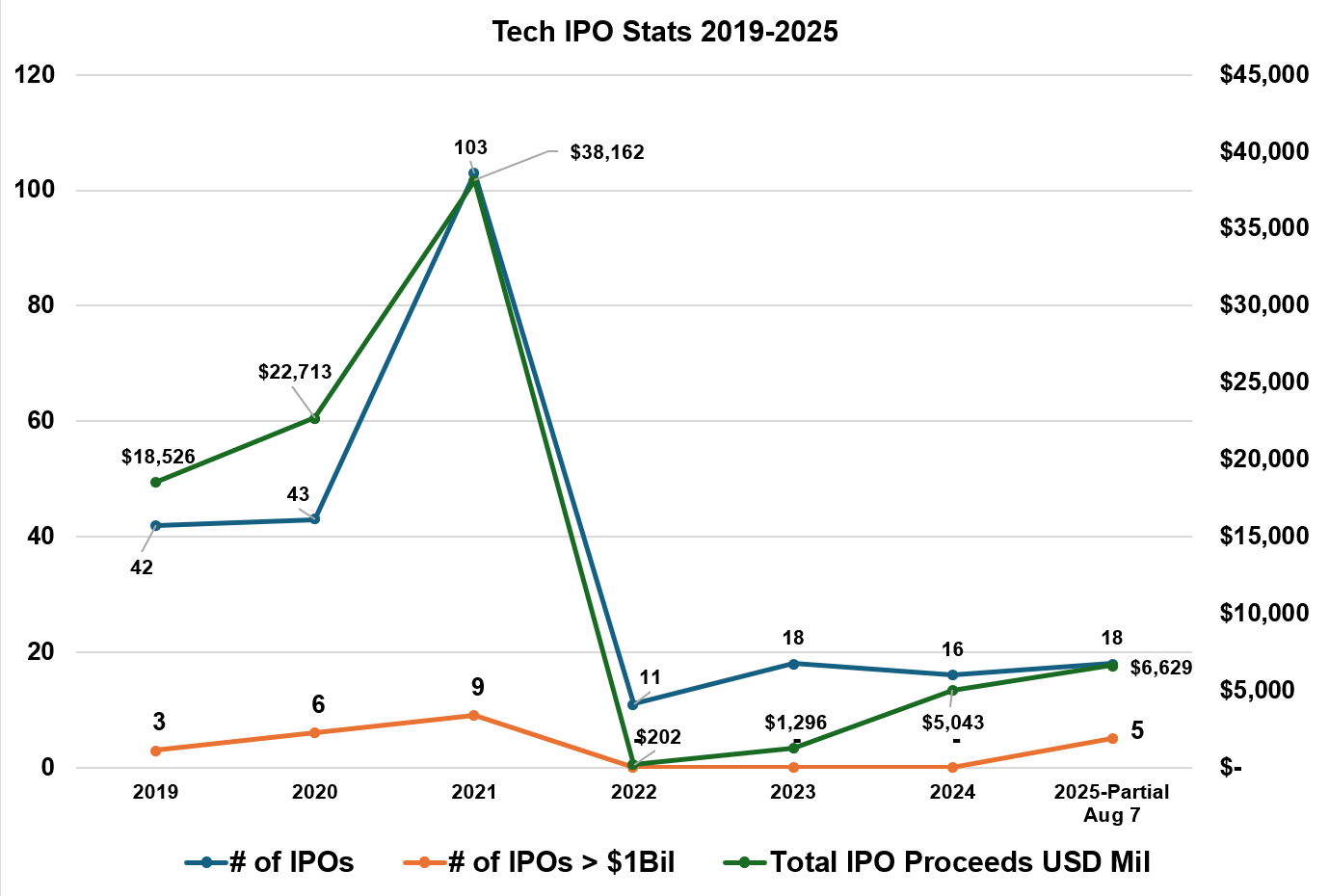

In 2019, 42 tech IPOs raised over $18.5 billion in total. Three of the 2019 transactions individually raised proceeds in excess of $1 billion. In 2021, IPO deal volume and value more than doubled to 103 transactions worth over $38 Billion, with nine IPOs raising more than $1 billion each. Then came a rapid rise in US interest rates and the IPO window effectively slammed shut and stayed closed in 2022-2024. Combined deal volume and value for 2022-2024 was smaller than the number and value of deals done in 2019 by itself. There were no tech IPOs from 2022-2024 that raised over $1 billion. This bleak period for tech IPOs was largely driven by subdued institutional and retail appetites for new issuances fueled by shifting interest rates. As a result, tech companies elected (or were forced) to stay private for longer or for good. Many reached cash-flow break-even or profitability and some have maintained relatively high growth (>20%) and while increasing profitability towards the mid-teens range. In some cases, the growth and profitability profiles are even higher. Data from recent MGI 360 Ratings in CLM, Billing, and CPQ markets aptly illustrate the strengthening trend towards greater profitability. The promise of Gen AI to raise productivity in software development, sales and marketing is also likely to influence the thinking of many tech founders when it comes to IPOs. Liquidity for early investors is always a consideration but not the only reason to pursue a public listing. Market visibility, improved ability to attract top talent and higher credibility with customers also factor into IPO decisions. IPOs are an important waypoint in the maturity of companies, not the end objective. Is the IPO window going to meaningfully open in the next 12 months? Very likely. Short of stagflation in the US, significant geopolitical or public health disruption, interest rates may moderate in the next 12 months. However, interest rate cuts are not certain, and more importantly, the re-opening of the IPO market and interest rate adjustments are not tightly connected. Independent of interest rate moves, investors look hungry. The recent Figma IPO was hugely oversubscribed, and the stock is trading significantly above the offering price. Last week, Firefly Aerospace, a rocket and lunar lander maker, raised $868 million and soared more than 30% on first day trading. Consistent with past opening periods, deal pricings have been set to feed investor appetites and stoke excitement in new offerings. Anecdotal evidence indicates investment banking teams are working unusually long hours preparing deals. This is at a time when most bankers are sipping cold drinks in the Hamptons. Board members who represent venture or private equity firms are eager for liquidity – they have limited partners clamoring for distributions. YTD 2025 data paint a picture of a strong recovery in IPO activity: Value of IPO deals so far (as of Aug 7th 2025) is greater than the value for all deals in 2022-2024 combined. This year already had five IPO transactions each raising more than $1 billion. Companies poised for an IPO exhibit very strong business profiles – typically with revenues exceeding $300 million, steady growth, and robust profitability. Soon to join the IPO pipeline is the Gen AI cohort demonstrating hyper growth. Given the data and mounting evidence, the IPO market is hotting up. There is a greater than 50% probability the IPO window will open in a very real way starting in September. Given the deep backlog of quality businesses coupled with the growth rates of some AI companies, the IPO boom cycle is poised to gather momentum. |

Research Spotlight

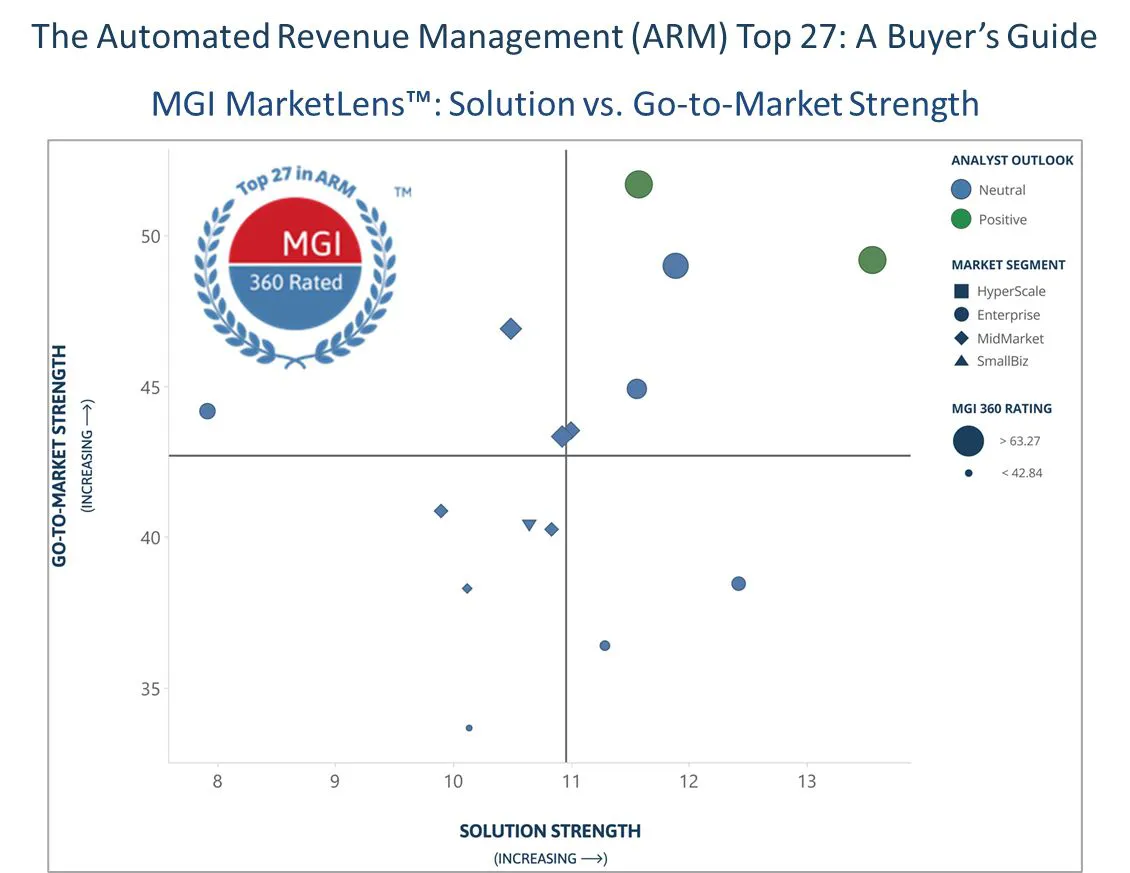

Is Your Services Quoting Process Holding You Back? |

|

|

Nearly 40% of first-time Services CPQ implementations fail, often due to poor vendor fit or underestimating complexity. The 2025 Services CPQ Buyer’s Guide is your roadmap to making smarter, faster decisions in a fast-changing market. Designed for services executives, sales ops, IT, and finance leaders, this guide outlines key trends, must-ask buying questions, and a breakdown of the top Services CPQ providers across Platforms, PSA Suites, and Point Solutions. It also introduces the MGI MarketLens™, a visual framework mapping CPQ depth vs. PSA breadth, helping teams quickly identify the best-fit vendors for their needs. Whether you’re modernizing an outdated quoting process or building your first shortlist, this guide will help you:

Don’t let outdated tools slow your services business down. |

|

|

So What Have I Missed?

|

|

|

That’s it for this issue of The Margin. If you’ve made it this far, we’ll certainly see you next time.

Warm wishes,

MGI Research