PSA Innovation at a Crossroads

The Professional Services Automation (PSA) software market is entering a period of supplier divergence. After more than a decade of vendor consolidation and incremental product enhancements, the focus today returns to innovation and bringing transformative capabilities to Professional Services firms. To help buyers, suppliers, and investors assess which vendors are leading in innovation and those keeping up or falling behind, MGI Research has created the PSA Market Innovation Map (MIM). This analysis plots PSA vendors by the markets they best serve and measures their degree of business and product innovation.

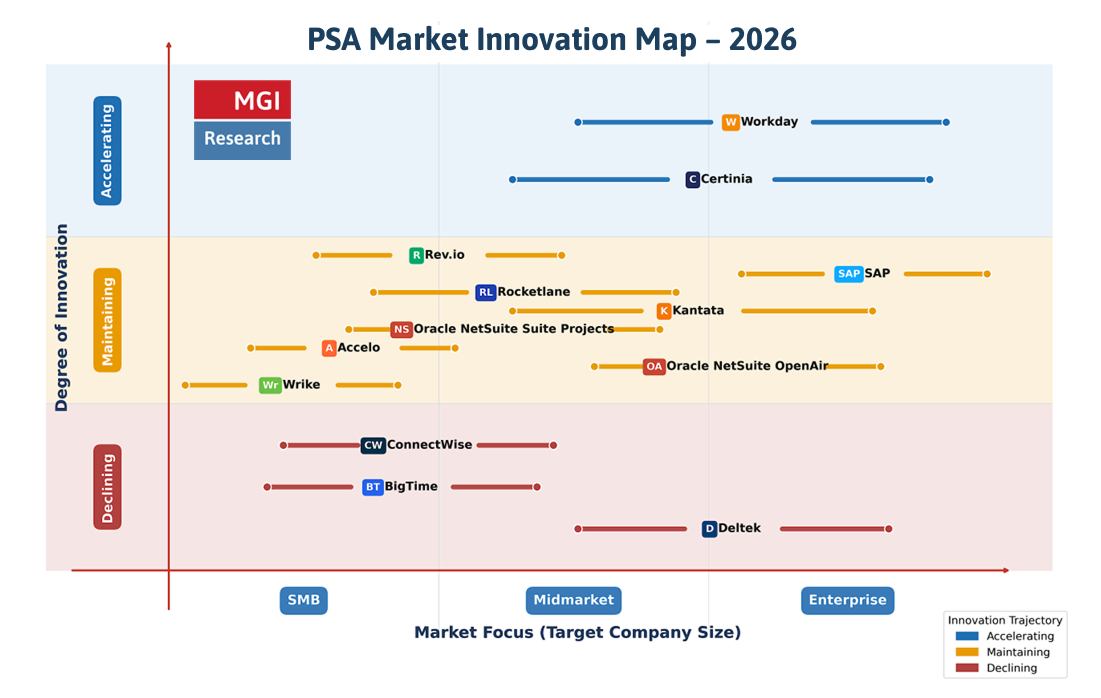

The PSA market today is characterized by three tiers: suppliers that are Accelerating, Maintaining, and Declining in pace of innovation. A small group of suppliers is leading the pack, introducing novel ideas and embedding AI into the core of key areas like resource management, revenue forecasting, and billing intelligence. A second group of vendors is not far behind, often limited by resources, creativity, or focus. A third group is falling behind, weighed down by legacy thinking, constrained finances, and emphasis on margin health over product advancement.

These vendor dynamics appear at a time when the stakes for Professional Services firms are quickly rising. Users are under mounting pressure to do more with less, and their future success hinges, in part, on the PSA solutions underpinning their financial and business operations. This note examines where PSA vendors stand in terms of their ability to deliver differentiated solutions and successfully meet increasing customer requirements.

MGI Research’s PSA Market Innovation Map plots 12 MGI 360 Rated™ PSA vendors across two dimensions: Degree of Innovation (Y-axis: Accelerating, Main-taining, Declining) and Market Focus by target company or use case size (X-axis: SMB, Midmarket, Enterprise).

Definitions:

Degree of Innovation

The extent to which vendors reimagine processes to increase efficiency, the delivery of new technology and approaches enabling net-new, transformative activities, and the extent to which these improvements are tailored to the needs of their ideal customer profile. Company performance in innovation is not be directly related to other MGI metrics such as Agility, Complexity, and Volume.

Accelerating

Frequent, substantive product releases, AI capabilities in production rather than preview, modern cloud-native architecture enabling AI to operate across a unified data model, and an ability to monetize AI as a premium tier.

Maintaining

Investment in AI at rates sufficient to remain competitive in evaluations, but fundamentally not reshaping their product architectures or creating durable differentiation. Releases include AI-adjacent features: enhanced analytics, predictive utilization dashboards, and integration improvements incorporating AI from underlying platform providers (Microsoft, Salesforce, Google) rather than building proprietary AI capabilities.

Declining

Product investment signals (e.g., release cadence, R&D announcements, customer review trends, and ownership structure) suggest platform management for profitability rather than advancement. These products were built for a previous era of buyer requirements and at risk of falling behind in the shift toward agentic AI, unified data models, and modern UX.

Leaders, Laggards, and Those in Between

The Leaders: Workday and Certinia

Workday and Certinia are beginning to distinguish themselves through their broad adoption of AI both internally as well as within their product and delivery capabilities. Over the last 12 months, both vendors have accelerated agentic AI feature rollouts across staffing optimization, forecasting, workflow automation, and analytics. Workday PSA leverages the broader innovations being developed by the company and benefits from a more narrowly focused ICP. Certinia’s Veda AI platform is nascent but signals an ambitious direction.

The Middle: Eight Vendors Keeping Pace

Rev.io, SAP, Rocketlane, Kantata, Oracle NetSuite Suite Projects, Accelo, Oracle NetSuite Open Air, and Wrike occupy a crowded middle tier. These vendors, varying significantly in size and R&D budget, share a common characteristic: they have yet to introduce market-defining approaches that materially reshape buyer expectations. Companies at the front of this cohort, e.g., Rev.io, SAP, and Rocketlane, display strong promise. Rev.io has rearchitected its entire platform and reengineered its development. SAP PSA takes advantage of the broader investment and innovation agenda of the overall company. Rocketlane, the newest and most modern of this triad, is the vendor to watch. For the rest, AI investments remain largely tactical rather than architectural, mostly surfacing capabilities from major industry vendors or major LLM providers.

The Laggards: Deltek, ConnectWise, and BigTime Software

Deltek, ConnectWise, and BigTime Software exhibit market signals — release cadence, R&D announcements, customer review trends, ownership structure — consistent with platforms managed for margin rather than advancement. ConnectWise represents a clear casualty of PE-driven over-consolidation. Under Thoma Bravo ownership, ConnectWise expanded aggressively through acquisition, yielding increased and unaddressed technical debt, and the PSA product has not seen a meaningful architectural or functional improvement in years. Similarly, BigTime struggles to evolve its platform in the face of rising buyer expectations. The Declining classification reflects slow product trajectory and bare-minimum investment. These are products not keeping pace with the rapid shift toward the use of agentic AI and accelerating automation.

The Next Wave of PSA Innovation

Professional Services as an industry is facing existential crisis. The way services and projects are priced, bought, staffed, and managed is changing radically. Firms’ individual survival will be dependent, in part, upon deploying modern tooling. The PSA Market Innovation Map (MIM) is one lens into this evolving vendor landscape. Firms evaluating PSA tools today should look beyond AI applications to existing workflows or industry standard infrastructure (e.g., MCP servers) and reach instead for suppliers demonstrating the capacity and creativity to redefine how services are delivered moving forward. Examples of new, innovative approaches to Professional Services include, but are not limited to AI-native resource and margin intelligence, predictive scoping and bid accuracy, cross-client portfolio intelligence, and billing and revenue recognition agility.

Ultimately, the opportunities for automation and fundamental transformation are only bound by human imagination and the capacity of suppliers to execute.

Conclusion

The market for PSA solutions is at an inflection point. Once a software category defined by incremental functional improvements, PSA today has become mission-critical for services firms seeking high operational control. The divide between innovation leaders and laggards among PSA vendors will likely widen over the next three years. Vendors treating AI as a surface-level enhancement will be displaced by competitors architecting entirely new approaches to predictive decision-making and autonomous operational workflows.

Go deeper: Readers requiring further analysis of how AI is changing PSA, broader market trends, and a risk assessment of PSA vendors should read MGI Research’s PSA Top 16 Buyer’s Guide — the most comprehensive analysis of PSA solutions and suppliers.