Executive Summary

Revenue leakage – the variance between contractually obligated revenue and actual recognized revenue – represents a fundamental failure in what MGI Research defines as the Agile Monetization Platform (AMP): the integrated business capability spanning pricing strategy, contract execution, fulfillment orchestration, usage measurement, billing operations, revenue recognition, and cash collection. MGI Research’s analysis of enterprises across a spectrum of industries, including manufacturing, professional services, telecommunications, healthcare, and technology, reveals material revenue leakage represents a pervasive control deficiency affecting the majority of companies of all sizes.

This control failure is not just an operational inefficiency – it is a material financial misstatement risk. Revenue leakage exceeding SEC materiality thresholds (5% of revenue, 10% of EBITDA)[1] puts a company in violation of ASC 606 (the accounting standard that defines how revenues should be recognized). This triggers SOX 404 – a demanding corporate compliance requirement for public companies to prove financial reporting controls work – potentially requiring financial restatement from the company.

This research note is the first in a five-part series. This note defines revenue leakage, and provides examples of what it is, and what it isn’t. To stop revenue leakage, individual companies and the broader business community as a whole need a common definition and understanding of this problem that represents at least three to five percent of every company’s revenue. This is the first research note in a multi-part series aimed at helping finance, business, and IT executives develop a consistent understanding of the problem, the risks of ignoring revenue leakage, and practical steps any organization can take to mitigate revenue leakage.

Key Findings:

Revenue leakage concentrates in three AMP capability gaps:

(A) Quote-to-Contract execution failures stemming from manual data transfers and approval bypass,

(B) Contract-to-Cash process breakdowns caused by system integration gaps between obligation fulfillment, billing, and financial systems, and

(C) Revenue Recognition control deficiencies reflecting inadequate ASC 606 compliance frameworks for complex multi-element arrangements.

MGI Research analysis identifies four permanent leakage mechanisms: billing windows closing before invoice generation, customer relationship termination before delivery-to-billing cycle completes, statute of limitations expiration on unbilled claims, and contractual barriers preventing retrospective billing. Each mechanism exhibits industry-specific manifestation but shares a common root cause: excessive cycle times in monetization processes create temporal risk that commercial opportunities close permanently.

The financial statement impact extends beyond understating income. Working capital distortion, cash conversion deterioration, and gross margin misrepresentation compound to create debt covenant risk, valuation compression in strategic transactions, and audit opinion qualification exposure.

Remediation follows three-phase methodology: diagnostic quantification (4-8 weeks), tactical process corrections (90 days, demonstrable near-term recovery), and strategic AMP capability buildout (12-24 months). Companies successfully remediating revenue leakage achieve substantial improvements in cash conversion, margin realization, and financial control maturity. Gains in these areas position the organization for consumption-based business model transitions and dynamic pricing strategies.

However, the strategic imperative transcends near-term financial recovery. Revenue leakage signals the inability to capture value proportional to value delivered – a fundamental monetization architecture failure. As enterprises transition from product-centric to outcome-based business models, monetization architecture becomes a strategic differentiator. Companies with mature AMP capabilities (i.e., real-time usage measurement, dynamic pricing execution, automated revenue recognition, proactive collection management) demonstrate superior cash conversion and growth scalability.

Definitional Framework: Revenue Leakage Within the Monetization Value Chain

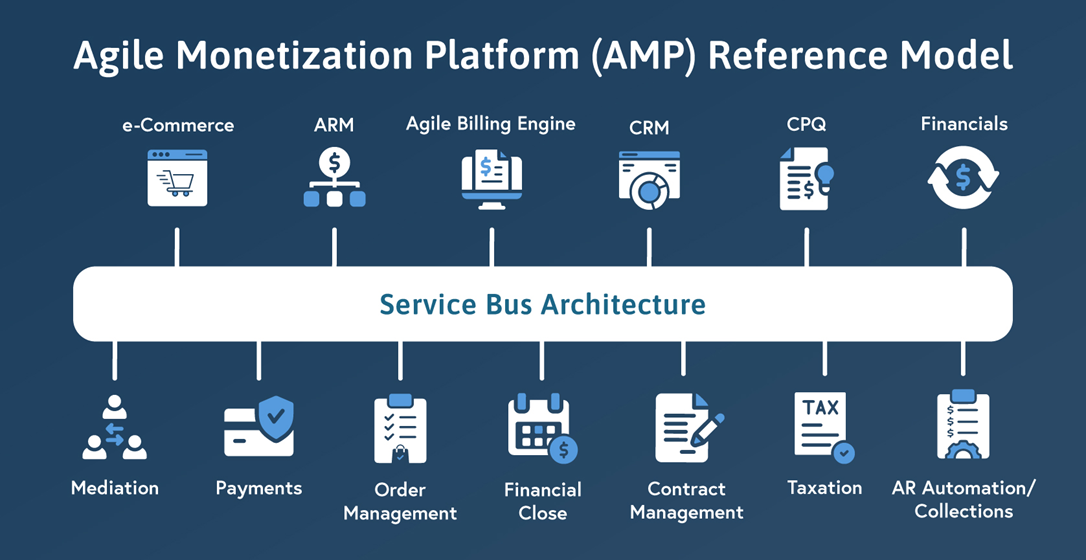

Revenue leakage is the measurable variance between revenue contractually committed by customers and revenue actually recognized in financial statements or converted to cash, caused by systemic failures in quote-to-cash business processes, revenue recognition errors, or inadequate financial controls. This definition situates revenue leakage within MGI Research’s Agile Monetization Platform (AMP) framework, which conceptualizes monetization as an integrated business capability spanning seven core processes:

AMP Reference Architecture

MGI Research’s AMP Reference Architecture details thirteen touchstones that every organization needs for successful monetization. The following is a list of functions within this architecture that pertain to revenue leakage:

- Pricing Strategy & Catalog Management: defining value metrics, price points, and packaging

- Configure-Price-Quote (CPQ): translating customer requirements into accurate quotations

- Contract Lifecycle Management (CLM): negotiating, executing, and managing contractual obligations

- Order-to-Fulfillment: orchestrating delivery of products, services, or access rights

- Usage Measurement & Rating: capturing consumption and applying tariffs

- Billing & Invoicing: generating customer invoices and managing billing cycles

- Revenue Recognition & Collection: accounting for revenue under GAAP and collecting cash

Revenue leakage manifests as process breakdowns within and between these AMP components. A manufacturing company shipping equipment under signed purchase orders but failing to correctly invoice installation services experiences billing leakage. A professional services firm delivering consulting hours without capturing time in tracking systems cannot bill for delivered work. A telecommunications provider metering customer usage but lacking integration between mediation and billing platforms cannot monetize consumption.

The definitional boundary excludes sales pipeline losses prior to contract execution (not leakage but conversion efficiency), negotiated discounts within approved pricing governance (intentional pricing decisions, not leakage), legitimate customer credits or returns (proper revenue reversals), and contractual terminations executed per agreement terms (churn, not leakage).

For further reading, see Revenue Leakage Series Part 3: The Geography and Mechanics of Revenue Leakage for more information on where breakdowns between the AMP Reference Architecture components take place.

Leakage Taxonomy by Financial Statement Impact:

Recognition Leakage: Revenue earned under contract but not recognized in financial statements due to accounting errors or systematic control failures. This directly understates the income statement and creates restatement risk when discovered. Recognition leakage stems primarily from ASC 606 compliance failures in identifying performance obligations, allocating transaction prices, or determining recognition timing.

Billing Leakage: Services delivered or goods shipped but invoices not generated within standard billing cycles. This creates contract assets (unbilled receivables) on the balance sheet and working capital strain, though GAAP revenue may be properly recognized if delivery triggers accrual under ASC 606. However, if billing delays extend beyond project completion or customer relationship termination, temporary leakage converts to permanent loss as retrospective billing becomes contractually or commercially infeasible.

Collection Leakage: Invoices issued but payment not received due to payment processing failures, inadequate dunning procedures, or customer credit deterioration. Collection leakage does not affect revenue recognition (invoice issuance satisfies recognition criteria for most transactions) but reduces operating cash flow and increases bad debt reserves.

Entitlement Leakage: Consumption beyond contracted limits without incremental billing or contractual enforcement. This represents foregone revenue rather than historical misstatement – services consumed without compensation. Entitlement leakage does not appear in historical financial statements but represents substantial opportunity cost.

Leakage Taxonomy by Permanence:

Temporary Leakage: Timing differences eventually corrected through subsequent billing or accounting adjustments. Primary impact: working capital strain, not permanent P&L loss. Examples include standard billing cycle delays, recognition timing corrections, and collection delays beyond standard payment terms.

Permanent Leakage: Revenue never recovered due to temporal or contractual barriers. This represents true economic loss – EBITDA that will never materialize. Permanence drivers include: (1) statute of limitations expiration (typically 36-48 months depending on jurisdiction and contract terms), (2) customer relationship termination before billing cycle completes, (3) project closure in project-based businesses before final billing, (4) contractual billing windows closing, and (5) commercial infeasibility of retrospective billing.

Industry permanence rates vary significantly based on the length of customer relationships, contractual structures, and business model characteristics. Professional services firms with project-based engagements experience higher permanent leakage rates than telecommunications providers with ongoing service relationships that enable forward-looking billing adjustments.

Continue to Part 2: Why Does Revenue Leakage Happen?

This report is part of MGI Research’s monetization architecture research program. For additional perspectives on monetization strategy and implementation, visit www.mgiresearch.com/research.

[1] A rule of thumb, while not codified, is accepted by the SEC as expressed within SAB 99.